U.S. Short Term Rental Tax Deductions: A Host's Guide

Unlock major savings with our guide to short term rental tax deductions. Learn how to identify and claim every expense to lower your tax bill and boost profits.

Disclosure: Some links in this article are affiliate links. If you make a purchase, we may earn a commission at no extra cost to you. This helps support our content.

Welcome to your no-nonsense guide to short-term rental tax deductions. When we first started hosting at our own places—a family home in Washington, D.C., and a couple of beach properties down in the Riviera Maya—we learned fast that understanding taxes is just as crucial as perfecting the guest experience.

So, what are short-term rental tax deductions? Simply put, they are the qualified business expenses you can subtract from your rental income, which ultimately lowers your tax bill. Think of it as rewarding you for running your rental like the small business it is.

Disclaimer: The following blog post is provided solely for informational purposes from the perspective of fellow short-term rental hosts. It does not constitute tax, legal, or financial advice. Tax regulations are subject to change and can vary depending on your specific circumstances and location. Always consult a qualified tax professional or advisor before making financial or tax-related decisions for your rental business.

Your Guide to Smarter Rental Tax Deductions

This guide is designed to cut through some of the confusion. We'll break down which expenses can reduce your taxable income and put more money back where it belongs—in your pocket. We'll cover the basics, clarify the differences between key expense types, and share practical advice you can use right away.

Our goal is to give you the confidence to manage your finances like a pro, turning tax season from a headache into a genuine strategic opportunity. It all starts with treating your rental like a real business. For more on that mindset, check out our guide on how to start your Airbnb business (and yes, it is a business).

Why Tax Deductions Matter More Than Ever

The short-term rental market has grown significantly, and that kind of growth gets attention. Governments have rolled out new tax policies, and in the U.S., hosts now have to report rental income over a certain threshold.

This increased oversight means having a proactive tax strategy isn’t just a nice-to-have anymore; it's a fundamental part of running a successful and sustainable hosting business.

For a deeper dive into maximizing your returns, this complete guide to rental property deductions is a great resource. While it's based in Australia, many of the core principles on tracking and categorizing expenses are universally helpful for hosts everywhere.

By getting a firm handle on your deductions, you can directly offset rising operational costs and reinvest in your property. Let's walk through how to make that happen.

The Most Common Deductions for Hosts

Alright, let's get into the good stuff—the expenses nearly every host can claim to lower their taxable income.

When we first started hosting, we quickly realized that tracking these everyday costs was everything. You have to think of these as the bread and butter of your short term rental tax deductions.

It can feel like a lot to keep up with at first, but once you get a system down, it becomes second nature. The key is to see every expense not just as a cost but as a potential deduction. From the mortgage payment to the extra rolls of paper towels you buy in bulk, it all adds up.

The Big Three Property Expenses

For most hosts, the largest deductions come from the costs of simply owning the property itself. These are your foundational expenses, and you absolutely can't afford to miss them.

Mortgage Interest: If you have a loan on your rental property, the interest you pay each year is typically fully deductible. Your lender makes this easy by sending you a Form 1098 that spells it all out.

Property Taxes: The taxes you pay to your local or state government for owning the property are another huge deduction.

Insurance: Your landlord or vacation rental insurance policy is a necessary business expense. Getting the right coverage is critical, and you can usually write off the entire premium.

These three expenses often represent the biggest chunk of your annual deductions, giving you a substantial offset to your rental income right from the start.

Day-to-Day Operating Costs

Beyond the property itself, you have all the costs that come with running a top-notch rental. These are your operational expenses—the things you buy and pay for to keep the business running smoothly and your guests happy.

Based on our experience, it’s helpful to break these down into categories, which makes tracking so much easier come tax time.

Below is a quick-reference table that categorizes some of the most common deductible expenses for hosts. Think of it as a starting checklist to make sure you're not leaving any money on the table.

Expense Category | Examples | Quick Tip |

|---|---|---|

Utilities | Electricity, gas, water, trash service, internet, and cable TV packages. | Pro-rate these costs based on business vs. personal use if you also use the property yourself. |

Supplies | Cleaning products, guest toiletries, coffee, tea, welcome snacks, lightbulbs. | Buy in bulk when possible and keep all your receipts in a dedicated folder or app. |

Professional Fees | Cleaning services, property management fees, accountant/lawyer fees. | The fees you pay to a CPA often pay for themselves through tax savings. This has certainly been true for us. |

Platform Commissions | Service fees charged by platforms like Airbnb, Vrbo, or Booking.com. | These are automatically documented in your platform payout statements, making them easy to track. |

Meticulously tracking these smaller, recurring expenses can make a surprisingly big difference in your final tax bill. For an even more comprehensive list of expenses you might be missing, this guide on the top rental property tax deductions for UK landlords offers some great insights, even if you're based elsewhere.

The goal is to build a clear financial picture of your hosting business. When you meticulously track every expense, you’re not just preparing for tax season; you’re gaining valuable insights into your profitability. This discipline was a game-changer for us.

By categorizing and logging these common deductions consistently, you'll be in a much stronger position when it's time to file. It transforms tax prep from a frantic scramble into a simple review of the numbers you've been collecting all year.

Repairs vs. Improvements: Understanding the Tax Impact

One of the first hurdles we ran into as hosts was the difference between a repair and an improvement. They sound similar, but the IRS sees them in completely different ways, and knowing which is which is a huge part of maximizing your short term rental tax deductions.

Here’s a simple way we think about it: a repair keeps your property in its current working condition. An improvement, however, makes the property better, more valuable, or extends its life. This distinction is absolutely critical for your tax strategy.

What Counts as a Repair

Repairs are all the necessary fixes that keep your property in good, safe, and rentable shape. The great thing about them is that they are considered current expenses. That means you can typically deduct 100% of the cost in the same year you pay for them, giving you an immediate reduction in your taxable income.

We learned this one firsthand after a big storm at our Playa del Carmen house knocked a few roof tiles loose. Replacing them was a clear-cut repair—we were just putting the roof back to the way it was before the storm.

Common examples of deductible repairs include things like:

Fixing a leaky faucet or a running toilet

Replacing a single broken window pane

Patching a hole in the drywall

Repairing a finicky appliance

Repainting a room to cover up scuffs and normal wear

When a Fix Becomes an Improvement

An improvement is a capital expense—a bigger project that adds significant value to your property, adapts it for a new use, or substantially extends its useful life. Instead of being deducted all at once, improvements have to be capitalized and depreciated over time, often on the same 27.5-year schedule as the property itself.

When we decided to do a full kitchen remodel at our D.C. house, that was an obvious improvement. We weren't just fixing a broken cabinet door; we were fundamentally enhancing the property's value and appeal to guests.

The IRS generally groups improvements into one of three buckets:

Betterments: Upgrades that materially add to the property's quality (e.g., swapping out old windows for energy-efficient ones).

Restorations: Major work that returns the property to like-new condition (e.g., replacing the entire roof structure, not just a few tiles).

Adaptations: Modifying the property for a new or different use (e.g., converting an unfinished basement into a new guest suite).

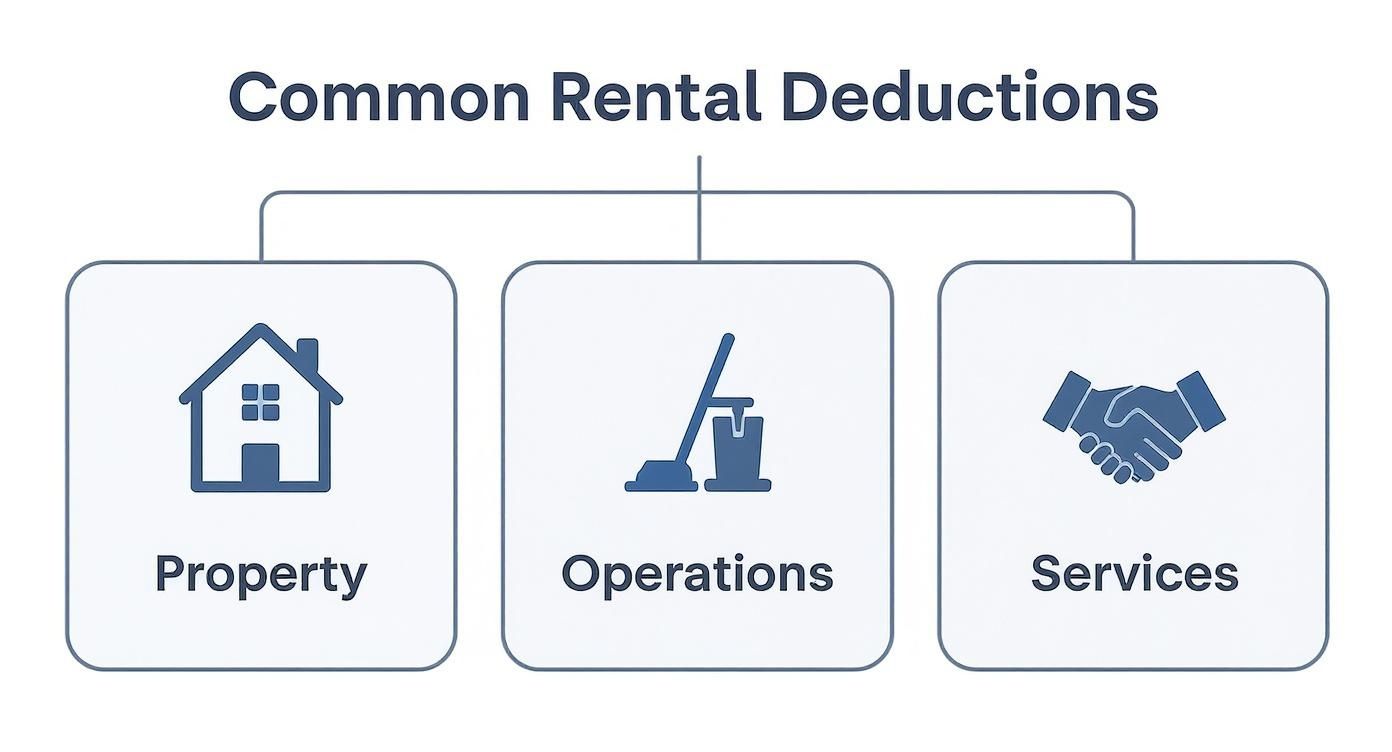

This decision tree shows the main categories of deductions, helping you visualize where expenses for your property, operations, and services fit in.

This visual helps clarify that all costs, from major property expenses to day-to-day operational supplies, play a role in your overall tax picture.

The key takeaway here is all about timing. Repairs give you an immediate tax benefit this year. Improvements spread that benefit out over many years through depreciation. Both are valuable, but they impact your cash flow and tax liability in very different ways.

Getting this classification right is fundamental to smart financial management. For a broader look at this, our guide on managing your vacation rental property offers more strategies for staying organized and profitable.

Our best advice? Keep detailed records with photos and receipts for every single job. It’s a simple habit that will make it much easier to justify your choices if you ever need to.

Unlocking the Power of Property Depreciation

Of all the short-term rental tax deductions out there, depreciation is easily the most powerful—and honestly, the most misunderstood. Think of it as a huge "on-paper" expense that accounts for the wear and tear your property and everything in it endures over time.

The best part? It’s a non-cash deduction. You don’t actually spend a dime in a given year to claim it, yet it can dramatically lower your taxable rental income.

For hosts, this is a total game-changer. It’s a way to recover the cost of your investment over its useful life, which directly boosts your cash flow by cutting down what you owe the IRS.

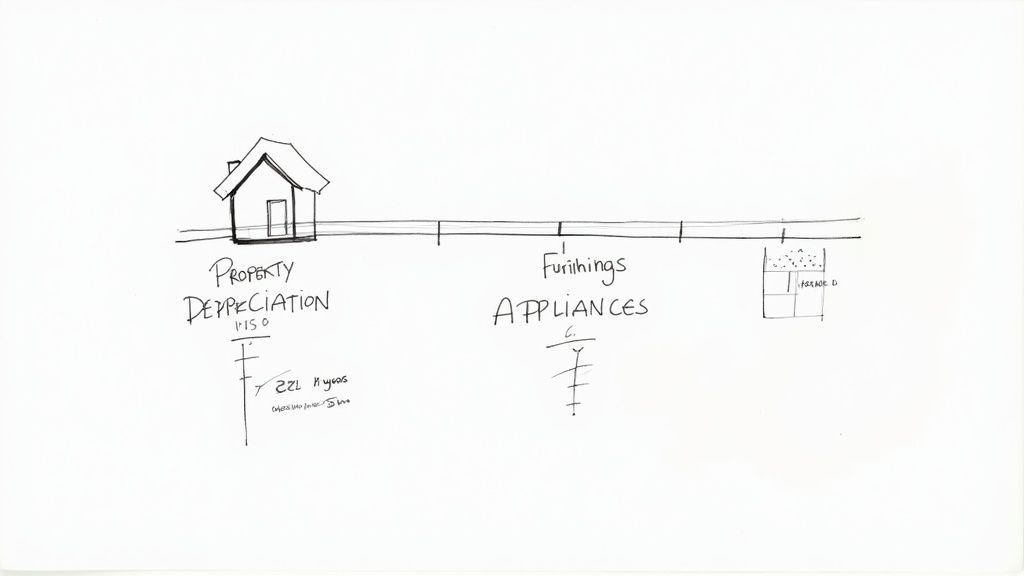

How Depreciation Works for Your Property

The IRS sets specific schedules for how long you can depreciate different assets. For residential real estate in the U.S., including your vacation rental, the building itself (the structure, not the land) is depreciated over 27.5 years.

To calculate your annual deduction, you take the property's cost basis—what you paid for the building plus certain closing costs, minus the value of the land—and divide it by 27.5.

Example in Action: Let's say you bought a condo for $350,000. An appraisal values the land at $50,000, leaving your building's cost basis at $300,000. Your annual depreciation deduction would be roughly $10,909 ($300,000 ÷ 27.5 years). That's nearly $11,000 you can write off without spending any actual cash that year.

This systematic deduction acknowledges that even a well-kept building ages, giving you a steady tax benefit year after year.

Depreciating Furnishings and Appliances Faster

Now, what about everything inside your rental? The beds, couches, TVs, and appliances that make your property feel like home definitely don't last 27.5 years. Thankfully, the IRS gets this and lets you depreciate these items on a much quicker timeline.

Most furniture, appliances, and equipment fall into a 5-year or 7-year depreciation schedule. This accelerated timeline means you can deduct the cost of these assets more quickly, giving you a bigger tax benefit in the early years of your hosting journey.

5-Year Property: This usually includes things like computers, cameras, and smaller appliances.

7-Year Property: This generally covers most furniture, fixtures, and larger appliances like refrigerators and washing machines.

For instance, a $10,000 investment in new furniture for your rental could create a $2,000 annual deduction for the first five years (using a simple straight-line method). You can see how these write-offs impact your overall numbers by plugging them into a vacation rental investment calculator.

Bonus Depreciation: A Game-Changer for 2025 and Beyond

Starting in 2025, hosts can take advantage of a powerful tax benefit that was recently made permanent. For qualified property—including appliances, furniture, and certain improvements—acquired after January 19, 2025, you can deduct 100% of the cost in the first year through bonus depreciation. This means that $15,000 spent on new furniture doesn't get spread over 5 years—you get the entire deduction immediately, creating significant cash flow benefits.

The Real-World Impact on Your Bottom Line

So, what does this all mean for your finances? When you combine the slow-and-steady depreciation of your property with the faster depreciation of its contents, you can create a massive paper loss that significantly reduces—or even eliminates—your taxable rental income for the year.

This is exactly why depreciation is one of the most strategic short-term rental tax deductions you can take. While it might sound complicated at first, getting a handle on it is key to running a financially smart rental business. From our experience, keeping a detailed asset list with purchase dates and costs is the absolute best way to stay organized and make the most of this powerful deduction.

Navigating Personal and Business Use Rules

Let's be honest, one of the perks of owning a vacation rental is getting to use it yourself. We love sneaking away to our place in Playa del Carmen for a few weeks every year. But when tax time rolls around, this is where things get a little tricky.

The IRS has specific rules about how you split expenses between your personal getaways and your paying guests. Getting this right is a huge deal if you want to stay on the right side of the tax code and maximize your deductions.

The Critical 14-Day Rule

So, how much personal use is too much? The IRS has a simple test to determine if your property is a rental business or more of a personal home that you sometimes rent out.

You cross over into "mixed-use" territory if your personal use is more than the greater of these two things:

14 days a year.

10% of the total days you rented it out to guests at a fair market price.

If you stay under that limit, the IRS generally sees your property as a pure rental business. This is great news because it means you can usually deduct all of your rental expenses, even if they create a loss.

But if you go over that limit, your property is treated as a personal residence for tax purposes, and the rules for deductions tighten up. In that case, you can typically only write off expenses up to the amount of rental income you brought in. You can’t use a loss from your rental to reduce your other taxable income.

A quick but important note: days you spend at your property doing major repairs or maintenance don't count as "personal use." If you're there for a weekend to repaint the deck or fix a leaky faucet, that's business time. Just make sure you document what you were working on.

Calculating Your Business Use Percentage

Once you've determined your property is mixed-use, you need to figure out exactly how to split your costs. You can't deduct the portion of your expenses that apply to your own stays.

The formula is pretty straightforward but absolutely critical:

Business Use Percentage = (Total Days Rented to Guests) / (Total Days Used for Any Purpose)

"Total Days Used" is simply the rental days plus your personal days. Any days the property sat empty don't factor into this calculation. This percentage is what you'll use for most of your big-ticket expenses.

Dividing Your Expenses The Right Way

Okay, let's put that percentage to work. Your expenses will fall into two buckets:

Direct Expenses: These are costs that are 100% deductible because they only happen when you have a guest. Think things like Airbnb or Vrbo service fees, advertising costs, or the supplies you buy exclusively for your guests. You don't have to prorate these at all.

Indirect Expenses: These are the costs that cover the whole year, no matter who's staying there. This is where you'll apply your business use percentage. We're talking about your mortgage interest, property taxes, insurance, and utilities.

Here’s a simple worksheet to show you what this looks like in the real world.

Category | Expense Description | Total Annual Cost | Business Use % | Deductible Amount |

|---|---|---|---|---|

Direct | Airbnb Service Fees | $4,000 | 100% | $4,000 |

Direct | Guest Welcome Baskets | $500 | 100% | $500 |

Indirect | Mortgage Interest | $12,000 | 90% | $10,800 |

Indirect | Property Insurance | $2,000 | 90% | $1,800 |

Indirect | Utilities (Total) | $3,600 | 90% | $3,240 |

Total Deduction | $20,340 |

In this scenario, the host rented their place for 270 days and used it personally for 30 days. That gives them a business use percentage of 90% (270 divided by 300 total used days). They apply that 90% to their indirect costs to get their final deductible amounts.

As you can see, keeping a meticulous record of your personal vs. rental days is non-negotiable. For us, having these dates clearly logged in our booking calendar and our vacation rental agreements is a habit that makes tax season infinitely less stressful.

Putting It All Together: Your Tax Season Action Plan

Knowing all the rules around short term rental tax deductions is one thing, but actually using that knowledge is what saves you money. Let's build a simple plan that makes tax time less of a frantic scramble and more of a strategic checkpoint for your business.

Trust us on this one: the key isn't cramming in April. It’s about building small, smart habits that you stick with all year long. After years of managing properties, we can tell you that getting ahead of your finances is the single best way to cut down on stress. A little organization now goes a very long way later.

Step 1: Get Obsessed with Record-Keeping

If you take only one piece of advice from this guide, make it this one: track everything. Every single receipt for cleaning supplies, every utility bill, every invoice from your handyman—it's all a potential deduction. Don't leave it until next spring to go hunting through old emails and bank statements.

Here’s a simple system that works wonders for us:

Get a Dedicated Business Account: Seriously, do this today. Funnel all your rental income and expenses through one specific checking account and credit card. It creates a clean paper trail and keeps your business finances separate from your personal life.

Snap Photos of Your Receipts: Use an app like Expensify or even a dedicated folder on your phone to take a picture of every paper receipt the moment you get it. This saves you from the inevitable lost-receipt panic.

Keep a Time Log: If you're aiming to qualify as a real estate professional or prove you "materially participated" in your rental, you must log your hours. Just a simple spreadsheet noting the date, the task (e.g., messaging with a guest, calling a plumber), and the time spent is all you need.

Step 2: Know When to Call in a Pro

While you can definitely handle the day-to-day bookkeeping, a good Certified Public Accountant (CPA) is one of the smartest investments a host can make. Their expertise is invaluable, especially when you get into more complex topics like depreciation or those tricky personal use rules.

Our advice? Find a CPA who understands real estate or, even better, short-term rentals. They’ll know the latest rule changes and can help you build a tax strategy that fits your specific goals. A good one can easily save you more than their fee.

You should definitely consider hiring a pro if:

You own more than one property.

You're trying to unlock advanced tax strategies.

You've just finished a big renovation or improvement project.

You just want the peace of mind that comes from knowing it’s all done right.

Step 3: Streamline Your Hosting to Win Back Your Time

Finally, the more you can automate your day-to-day hosting tasks, the more time and mental energy you'll have for the stuff that actually grows your business—like managing your finances. Smart tools don't just simplify your workload; they create the space you need for bigger-picture thinking.

For example, a tool like SmoothStay helps you create a customizable, professional guidebook, which can slash the time you spend answering the same guest questions over and over. That’s dozens of hours a year you get back to review your books, track expenses, or plan your next move with your CPA.

When the guest experience runs smoothly, you're free to run a more profitable and far less stressful business.

Common Questions About STR Deductions, Answered

As hosts ourselves, we know that once you get into the weeds of short-term rental taxes, a lot of specific questions pop up. Let’s clear up a few of the most common ones we hear from fellow hosts.

Can I Deduct Travel Costs to My Rental Property?

Yes, you can—as long as the trip is primarily for business. If you’re flying or driving to your rental to handle repairs, meet a contractor, or restock supplies, those travel expenses like airfare or mileage are generally deductible.

The key here is being honest about the trip's main purpose. If you're mixing a weekend of maintenance with a family vacation, you can only write off the costs directly tied to the business part of the trip. It's smart to keep detailed notes on what you did each day to back up your claim.

What Happens If My Rental Expenses Exceed My Income?

When your deductible expenses add up to more than your rental income for the year, you’ve got a net rental loss. Whether you can use that loss to offset other income (like the salary from your day job) boils down to the IRS's "passive activity loss" rules.

By default, rental activities are considered passive, which often limits your ability to deduct those losses against other income. However, if you "materially participate" in running your rental, you might be able to treat it as a non-passive activity and take the full deduction. These rules get complicated fast, so this is a perfect time to chat with a tax pro.

Do I Need to Issue a 1099 to My Cleaner?

This is a big one that catches a lot of hosts off guard. For 2024 and 2025, if you pay an independent contractor—like your go-to cleaner, landscaper, or handyman— $600 or more during the year, you'll generally need to send them a Form 1099-NEC. Note that starting in 2026, this threshold increases to $2,000.

There are a few exceptions. This rule usually doesn't apply if you pay them through a third-party platform that handles reporting (like PayPal Goods & Services). It also doesn’t apply to payments made to corporations. The important thing is to track all your direct payments to individuals so you don't miss this at year-end.

At SmoothStay, we're hosts building tools for hosts. We believe that simplifying your day-to-day tasks frees you up to focus on the financial health of your business. Our AI-powered digital guidebooks cut down on repetitive guest questions and create a seamless experience, giving you more headspace for big-picture strategies like maximizing your tax deductions.